Market Recap for Thursday, April 11, 2019

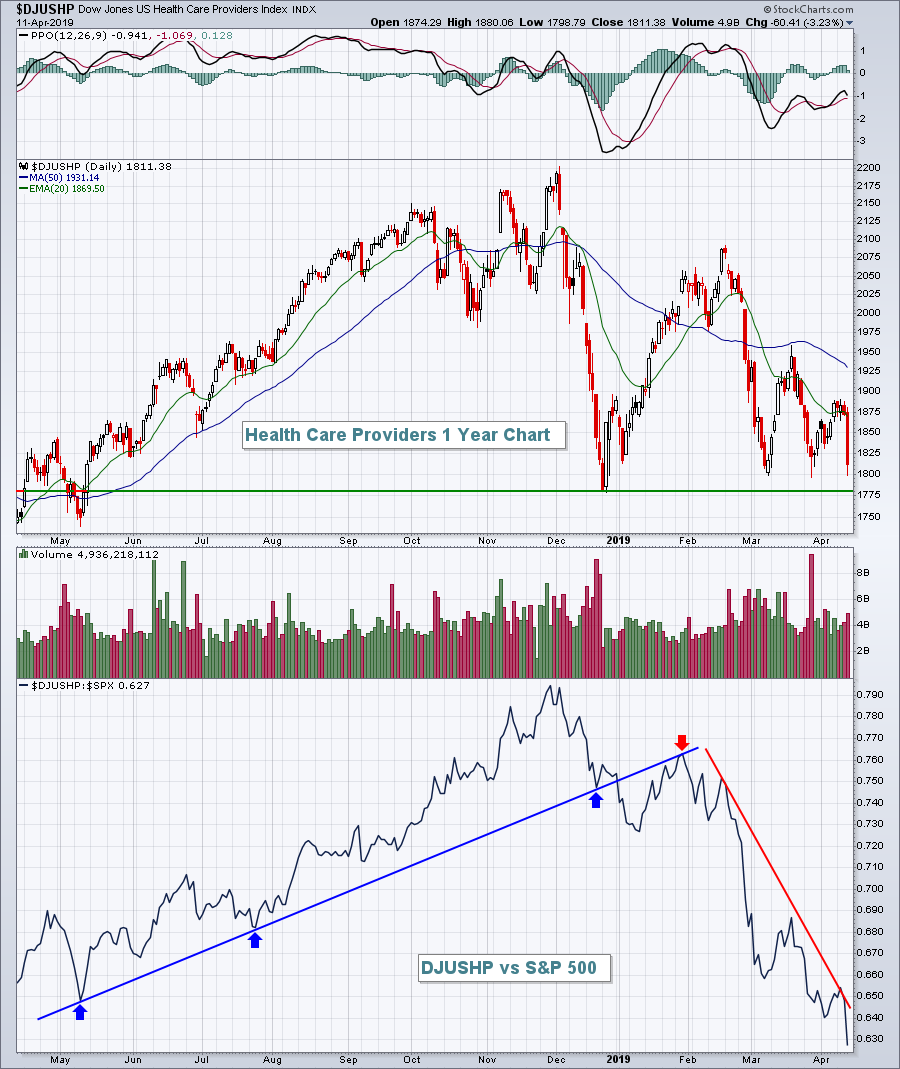

U.S. equities finished in bifurcated fashion as a late day rally enabled the S&P 500 to eke out a miniscule 0.11 point gain (+0.00%). The other major indices finished in negative territory, led by the 0.21% decline in the NASDAQ. Healthcare (XLV, -1.23%) was the primary reason for yesterday's lethargic action as health care providers ($DJUSHP, -3.23%) and biotechs ($DJUSBT, -1.56%) delivered the bearish blows. The former was a Wall Street darling in 2018, but has fallen apart in 2019 as you can see below:

The DJUSHP was clearly leading the S&P 500 higher in 2018, but its underperformance in 2019 has been remarkable and is currently showing no signs of letting up. Until we see a return of relative strength, it's best to avoid this group.

The DJUSHP was clearly leading the S&P 500 higher in 2018, but its underperformance in 2019 has been remarkable and is currently showing no signs of letting up. Until we see a return of relative strength, it's best to avoid this group.

Another weak area on Thursday was gold ($GOLD, -1.57%), which is quickly returning to a key price support level:

The 1280-1290 level really needs to hold or we could see much lower gold prices during the balance of 2019.

The 1280-1290 level really needs to hold or we could see much lower gold prices during the balance of 2019.

Industrials (XLI, +0.86%) and financials (XLF, +0.60%) were the sector leaders on the session. Insurance companies were quite strong, benefiting the financials.

Pre-Market Action

The first big bank reporting seemed to say everything is okay in banking as JP Morgan Chase (JPM) is up roughly 2% in pre-market trading. The giant reported EPS that exceeded expectations (2.65 vs 2.32) in an industry that was expected to deliver disappointing quarterly results. Maybe JPM is an outlier, but at least for a day the group appears to have avoided potential earnings-related issues.

The 10 year treasury yield ($TNX) is jumping 5 basis points this morning to 2.55%, a key short-term yield resistance level. Crude oil ($WTIC) is up 1.5% this morning and nearing $65 per barrel. Asian markets were once again mixed overnight, but there's a bullish bias in Europe this morning.

An announcement helping to boost U.S. equities is Chevron's (CVX) plans to acquire Anadarko Petroleum (APC), providing a premium of roughly 37% above APC's closing price on Thursday.

Dow Jones futures are taking their cue from JPM and other banks, rising more than 230 points with 30 minutes left to the opening bell.

Current Outlook

Yesterday, I provided a long-term bullish channel on the S&P 500. Today, let's review the more volatile Russell 2000. Its lower uptrend line actually connects the major lows beautifully. Drawing that same sloped line and connecting the 2014 high provides us a potential target within a channel as we move throughout 2019 and beyond:

I know everyone has their own opinion as to where we're going from here, but the above chart suggests this secular bull market lives on. When trendlines like the above break to the downside, then we have problems. Until then, I'll be biased to the upside.

I know everyone has their own opinion as to where we're going from here, but the above chart suggests this secular bull market lives on. When trendlines like the above break to the downside, then we have problems. Until then, I'll be biased to the upside.

Sector/Industry Watch

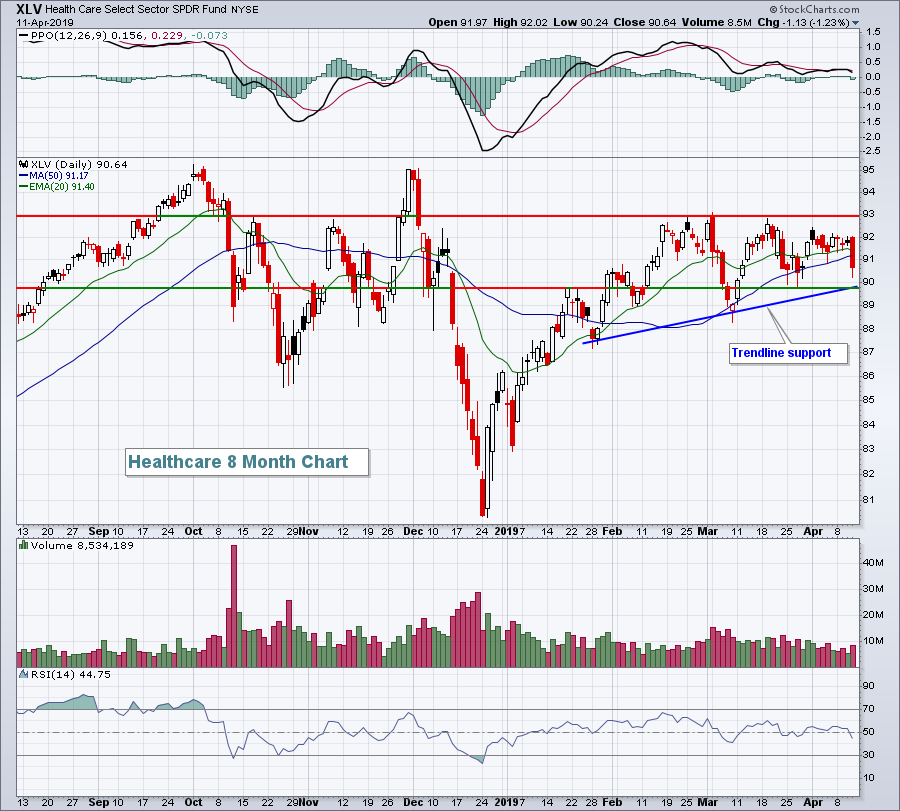

Healthcare (XLV) had a rough day on Thursday and is threatening its key 2019 trendline support as follows:

The 89.75-90.00 level has provided excellent price support over the past five weeks, and trendline support now intersects at that level as well. I'd be looking for a bounce in healthcare shares from this area.

The 89.75-90.00 level has provided excellent price support over the past five weeks, and trendline support now intersects at that level as well. I'd be looking for a bounce in healthcare shares from this area.

Historical Tendencies

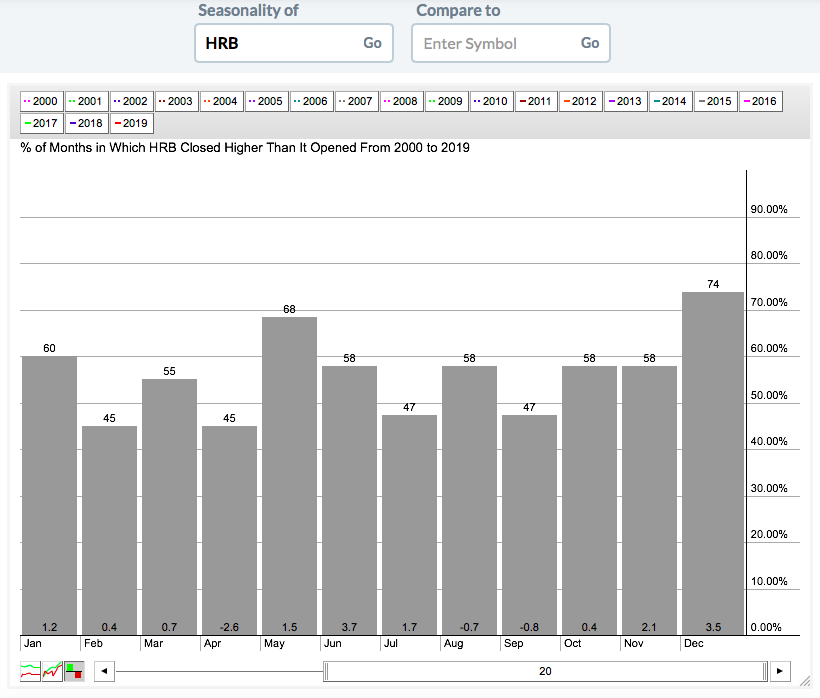

Somewhat surprisingly, H&R Block's (HRB) worst calendar month of the year is April, where it's historically failed to uncover the stock market's loopholes:

Its average loss of 2.6% during April is far worse than any other month's average returns. While you might consider HRB for your taxes in April, I'd think twice about buying their stock.

Its average loss of 2.6% during April is far worse than any other month's average returns. While you might consider HRB for your taxes in April, I'd think twice about buying their stock.

Key Earnings Reports

(actual vs. estimate):

FRC: 1.22 - estimate, awaiting results

INFY: .13 vs .13

JPM: 2.65 vs 2.32

PNC: 2.61 vs 2.59

WFC: 1.20 vs 1.08

Key Economic Reports

April consumer sentiment to be released at 10:00am EST: 98.0 (estimate)

Happy trading!

Tom