You need to imagine being on a tee-box playing golf with me. It seems that, every hole, we talk about a different dynamic in the markets. Because each market participant uses different ideas to analyze the market, it makes a lively discussion; industries to be in, how things have changed, the change in the leadership stocks and our latest humbling trade. Most don't like to discuss losses, but all of us like to shine a light on what has been working.

Different Investors

Let me give you an example of the different types of investors I chat with. One of these investors has one stock he continuously trades, but most of the investment capital is in a managed portfolio. Another has been in Fisher investments, because they don't invest in oil and gas and prefer tech. Another is into vegan foods, while another is an ESG investor. Others are retired, in dividend investing strategies, unaware of the market cycles and gyrations but watching their portfolio balance change. Others operate businesses, and the markets are a place to move intuitively in and out of the market, for challenge more than income. Another is a retiree, investing in Motley Fool stocks to do well over the long term.

Almost all have widely diverse portfolios, with their latest investment the focus of the discussion. Portfolio managers come with their own set of parameters. Dividends, diversification, slightly outperforming the indexes. Others are fundamental investors, analyzing future projects and financials, and they enjoy the company story as their primary investment driver. Then there are raw technicians, focused on a chart. Perhaps, as you read through the list, you can find the one that represents you.

After the round of golf yesterday, I was sitting on the deck with family and friends. The after-game is always enjoyable, and the 19th hole is the best part of a round of golf if you are not hitting it straight. I have some great friends with a boatload of different experiences surrounding me. But what is even better is the dialogue we share as investors, with our career backgrounds creating our biases. We also maintain a healthy respect for our differences of opinion, as that's what makes a market.

One of the most provocative statements for me, sitting on the deck yesterday from a fellow investor that I respect, was,

'Gas Prices Have Topped This Week.'

I am pretty sure my eyes did the ol' deer-in-the-headlights emoji 😳 .

I wasn't involved in the pricing of gasoline/diesel in the early 80s. I did live through the trauma of government involvement in the oil business back then. We could be headed to this political juncture again. A Senator announced a windfall profits tax on Wednesday, thinking that would cure the issue of high prices. It might be good for the political base, but the charts below lay out a different problem.

I want to work through the supply and demand situation for oil and gas. I think you'll find it informative while wondering about high prices. There are three main products that help set the stage: gasoline, distillates and crude oil. The charts provided by the EIA are publicly available on their website.

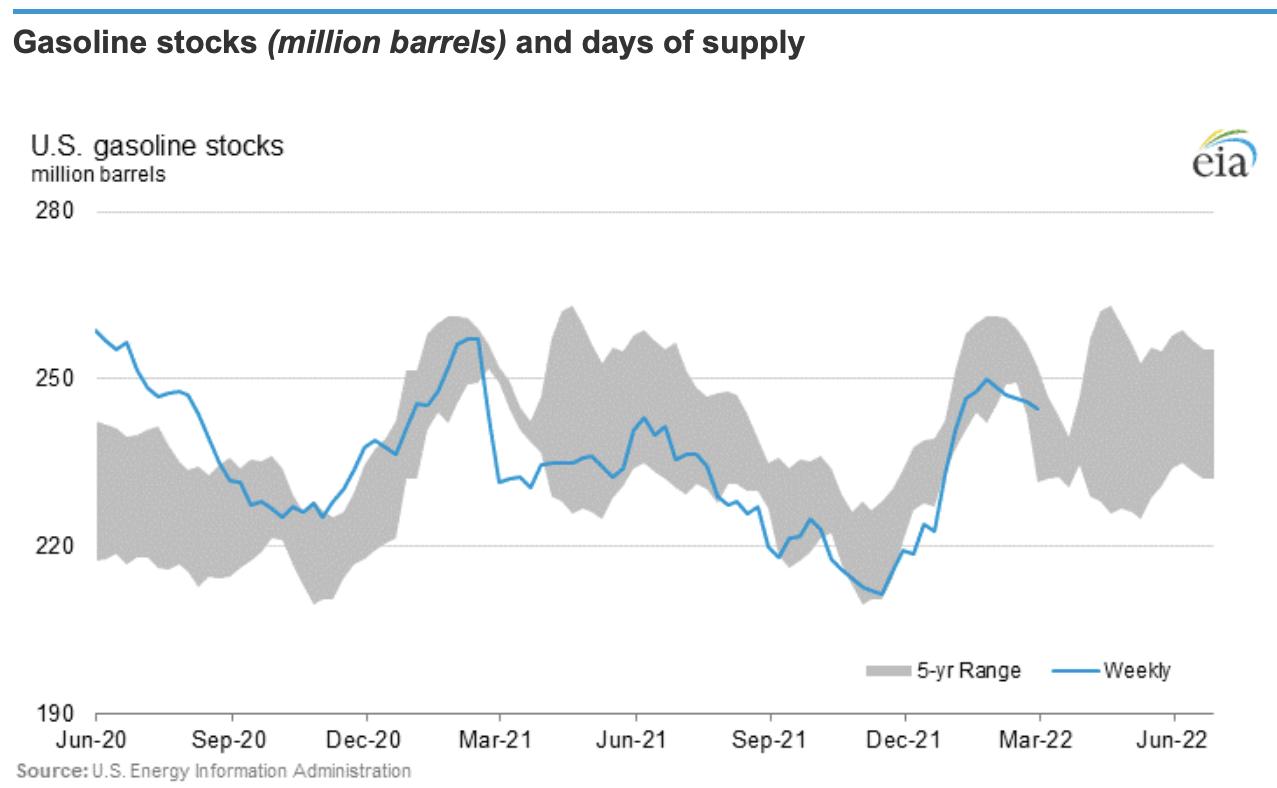

Gasoline

First of all, the chart for gasoline inventory ebbs and flows. The five-year range is the gray-shaded area and the bright blue line is the current level of inventory. This hides any supply situation really well, as everything looks normal. In my opinion, the shaded area doesn't deviate by a lot as it doesn't get really wide. The 5-year operating range is narrow. Refiners are aware of gasoline demand through the annual cycles required to keep gas stations supplied with gasoline.

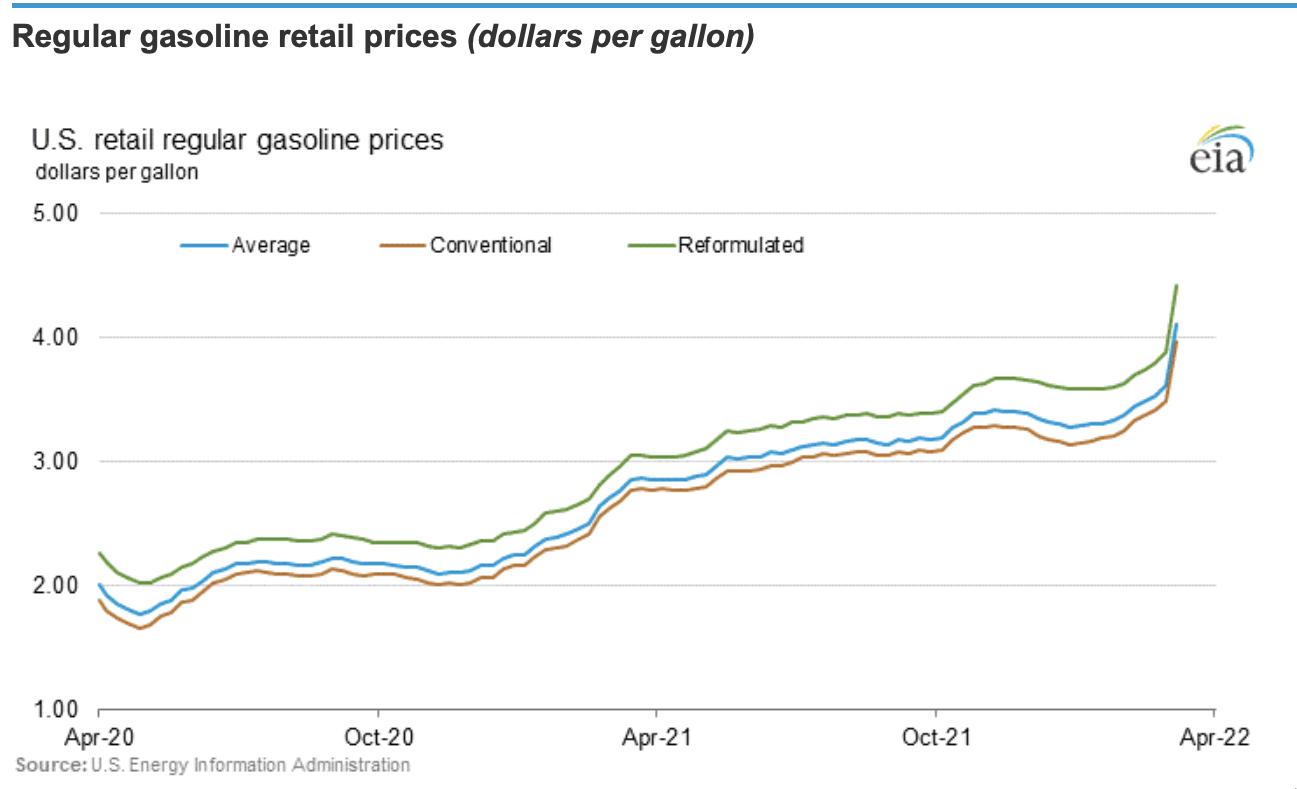

So does the price track gasoline inventory levels? The price chart makes a clear case that the graphic above does not create the chart below. The price has recently spiked, but inventories are in the middle of the 5-year range.

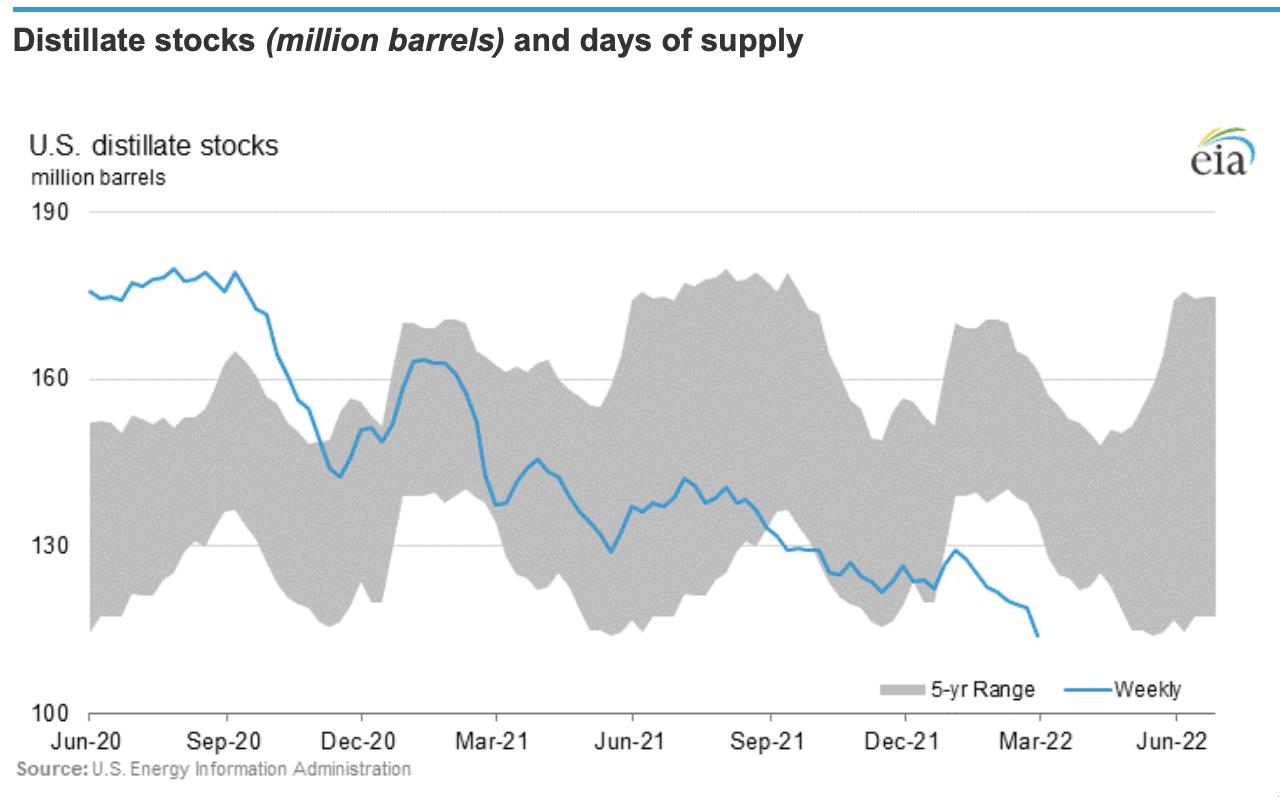

Distillate (think diesel fuel for simplicity)

The second main product out of a refinery is distillate. This can be highway diesel fuel, heating oil, kerosene or jet fuel. The chart captures the last 24 months in the 5-year shaded area, as well as showing the inventory levels (blue line) over the last 21 months. This line chart just broke below the 5-year lows for inventory, but was very close to the lows since October of last year.

One of the main data points for me on the chart is the blue line, which tried to cycle higher during both the December 2020 and June 2021 swing highs on the grey background chart but never made it up to the top of the range after being well above in June 2020. On the recent December 2021 swing high, it never got off the lows. That is a dramatic change. The trend is top left to lower right, consistently.

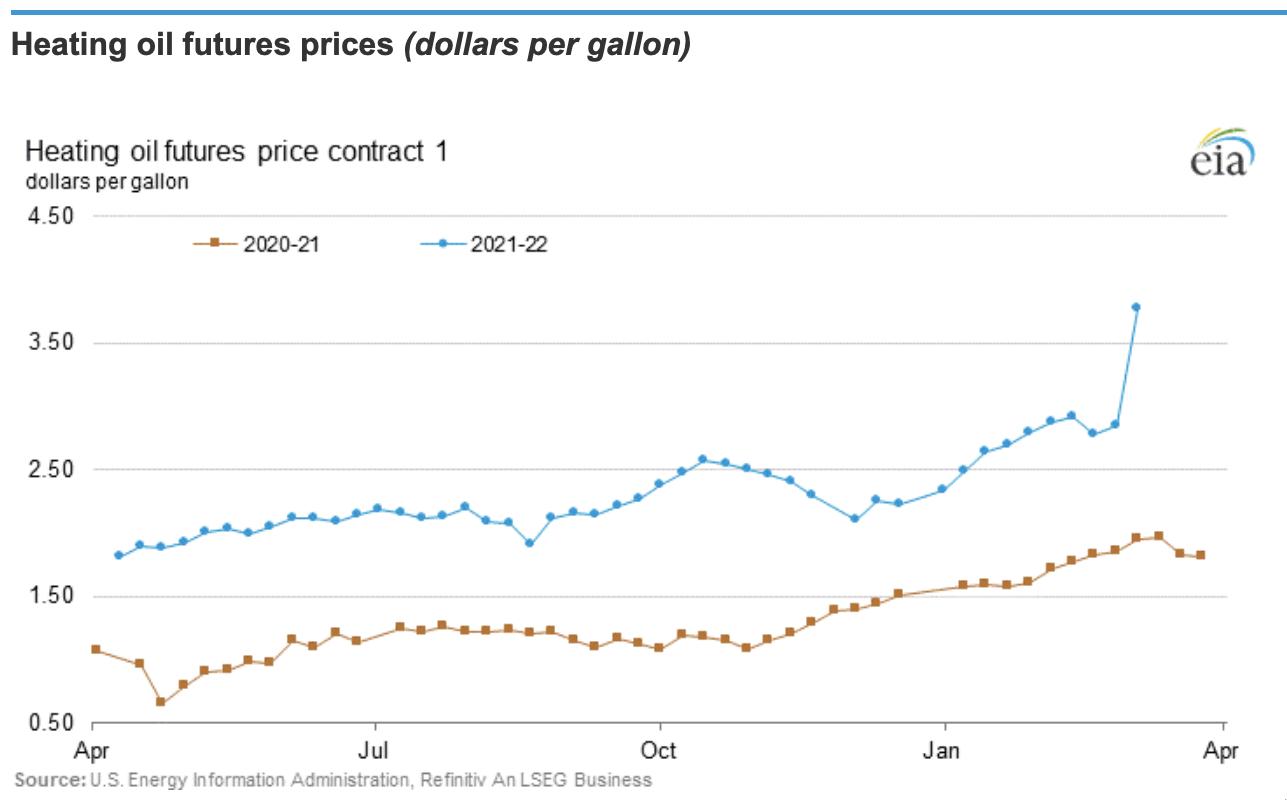

What have distillate prices done? This is a wraparound chart. The COVID lows are on the brown line in the bottom left. Prices rose from that low to around $1.75 in March 2021. The starting price for the blue line is the week following the end of the brown line. Again, the trend is up. However, the recent price spike that occurred on the gasoline chart above is even more obvious on the distillate chart. The main point here is that inventories have been declining for almost 2 years on the graphic above and are well below the seasonal lows as well as the five-year lows. In this product line, the inventory declines have been illustrated in higher prices. Supply/demand.

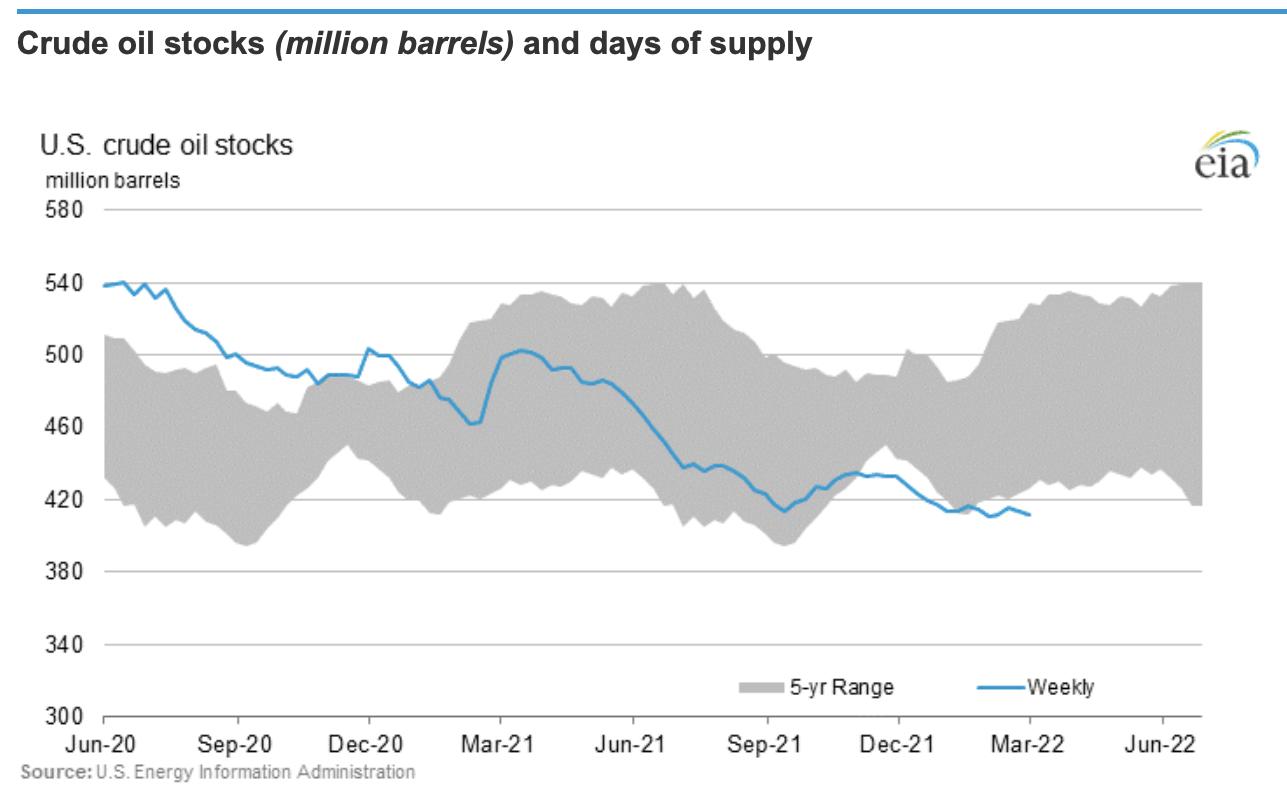

Crude Oil

We have one more liquid product to examine, that being crude oil. Notice the wide range from 400-520 over the last five years. This 5-year average is centered around 460, but there does not appear to be strong seasonal swings. The five-year range also includes the high 2020 inventory levels when the world unexpectedly stopped moving. Since November, we have been below the 5-year average almost every week. We started with 540 million barrels in inventory in June of 2020 and currently have an eyeball estimate of 410 million barrels. For rough calculations, inventories have dropped 20%.

What makes this more concerning is the 5-year historical lows are near this level. If we start to breach those lows and move down towards 380, that adds more pressure.

When we look at the price of oil, it is doing the same thing as distillates. It is reflecting the lowering of inventory, or, put another way, the tightness of supply. Supply/demand in its simplest form.

Strategic Petroleum Reserve

The strategic petroleum reserve was put in place to supply oil in times of war. We have been withdrawing from the SPR for quite a while now and, with the Russia/Ukraine conflict, perhaps the removal of oil in storage gets closer to a reason to do so, but so far the USA is using it as a price control mechanism. The SPR makes up about 6 days global supply and 30 days of US consumption. There are existing reservoirs continuing to produce, so the SPR is currently just knocking the edge off the low production and holding down price increases. Last week, a 2 million barrel draw from the SPR merely cushioned the huge product draws from inventory. This is not effective as a long-term solution, but can help briefly.

Global Pressures

With the sanctioning of Russia's oil supply to the global market, this adds new pressure. Global inventories, as well as US inventories, have been declining for two years, not two weeks. This decline in inventory was not due to the war.

So what would cause global inventories to decline so rapidly and why aren't oil companies doing more to increase supply? Put simply -

When was the last time the oil business was thanked by a politician for increasing supply?

In North America, the political wind is to get rid of the oil and gas industries because they create greenhouse gas emissions. The environmental perspective continues to dance on, increasing the force of wind and solar providing our energy needs. In Europe, the same green wave political forces are also in charge. Whether this is good or bad is not the purpose of this article. It is recognition of the current state of affairs.

In China, Russia and India, the environmental forces are not in play. While there is some renewable development going on, it is still a important policy choice to make sure their countries have reliable, low-cost energy. The countries with access to affordable energy are the most developed countries in the world and they want to be part of that list.

Global Inventories are Still Declining Every Week

So below is a list of the reasons why oil companies are not developing new oilfields at a faster rate. There is an old saying that the cure for high prices is high prices. This implies that as prices rise, production increases and slows the price increases. This eventually marks a top by creating a surplus as supply overwhelms demand, pushing prices back down.

Oil is the most traded commodity in the world. There are millions of factors involved in the price of oil, but the consistency of supply is one of the foundations.

Feel free to agree/disagree with each one of the points, but trust me, you don't have to email me. I have family members, friends and neighbors happy to tell me I am all wrong. These line items are my assessment with some limited industry background. I may have errors and omissions.

The key message is global inventories are declining every week. The Middle East has little spare capacity, but the commonly-held view by media is they have abundant barrels to put on the market. Most of the leaders in the Middle East have said the world is entering a dramatic shortage of crude and they cannot make up the difference.

Social issues:

- As long as oil is cheap and the companies are going broke, everyone loved dumping on them. As prices go higher and the need for oil holds up, consumers blame the oil companies. Now oil is expensive and the companies and the employees are still the devil. This is a primary problem why the industry cannot attract new people.

- Mainstream media loves to rip into the oil companies as the environmental villain. The world as a population has been iteratively reducing the damage to the environment each and every year for 80 years across numerous industries including power plants, manufacturing centers, textile plants and more. Oil companies have always been a focus and have adapted to change, and I have listed large-scale changes below, with no real appreciation from the media. This shapes the views of the people absorbing the media information.

- The media have largely trashed or ridiculed anyone working in the oil patch as ignorant, as working to kill off the environment. The companies are filled with smart people, trying to do better every day. There is not an industry on earth spending more annually on improving the environment than the oil business.

- Many of the Petroleum Engineering schools for Oil and Gas have been shut down, with pressure from government, ESG, alumni and students moving to more appreciated industries.

- When was the last time you thought positively about the people working in the industry? How does that compare with software? Wind and solar? Two of the largest data processing centers in North America were Houston and Calgary, and used computers for processing 3D models of the earths layers under the surface. This might have changed now, but they were some of the largest players in the development of computing systems. They have been a big part of positive change in the world.

- Everyone wants the environment cleanup done yesterday with little acknowledgement it is a game of moving goalposts. We as citizens of the world are never done and probably never will be done as we use the resources of the earth from water, plants, minerals and liquids. Even if there has been some improvement, there is not an environmental body willing to acknowledge the gains being made. It is always we must do more, and we must do it yesterday and make villains of the companies on the path of the crusade. At some point, the oil companies are our partners in life, giving us the products we want, while continually trying to diminish the impact on the planet. Today, the oil company is still the primary villain. It's an old story, but told by every generation driving around with gasoline in the tank, using natural gas in their homes heating water for warm showers and furnaces for cold climates.

- The Globe and Mail - a Toronto-based publication - only two weeks ago said oil business was dying a slow death. Who would invest in a business going to zero? Would this motivate you to apply to work in the industry?

- It wouldn't surprise me if staff levels at oil companies are down from last year as the stocks vest at new highs. This allows retirees to step out with their stock options and shares vesting at fresh new highs.

Financing of Oil and Gas

- Banks are not funding oil and gas projects

- Caisse Depot, OPP, CPP, CALPERS are all declaring they won't invest in oil and gas. The Norway Government pension plan goes out of its way to say every year they are discontinuing investment in oil and gas. Why they have to say it every year is a great question.

- Oil demand continues to rise significantly year over year. The decline has not happened.

- Little or no megaprojects globally. These used to be the cornerstone of keeping up with depleting reservoirs. Trying to get approvals for $40 billion projects with inconsistent government priorities and suppression of the industries means the companies are not willing to spend/invest money in long-term projects that may never be allowed to be completed. This is not just oil and gas. BHP and RIO just had a permit denied for a copper mine after spending almost $2 billion to get it to the permit stage.

- Russia/China positioning to control global commodities makes global trade difficult.

- If the Oil and Gas companies don't return money to shareholders, they won't get investors.

- Small drilling is being done, but not on a scale to keep up with the global declines.

- Wells in British Columbia, Canada can't be drilled due to recent First Nations court ruling.

- Canadian Mega-projects like TMX $14B, Coastal Gas $40 B, Keystone XL all get cancelled/delayed for years, making large-scale projects unattractive.

- Who will invest in new Newfoundland Offshore Oil and Gas projects as the Canadian government, including the Natural Resource Minister, are against developing new Oil and Gas projects. This in a country with the 3rd-largest reserves in the world.

- Similar problems exist across the USA trying to get big projects approved.

Some Good has Come from Oil and Gas Development

The reason for some of the cellular grid network into more remote parts of the North American surface area has been on the back of the remote location development for oil and gas, or natural resource development.

Below are some of the simple examples of environmental improvements that require massive investments to change existing systems.

- Smog was a big factor and the cloud over cities was an obvious problem as transportation with hydrocarbons increased.

- Years ago it was sulphur or acid rain. Low-sulphur diesel became a thing.

- Lead was in the gasoline to soften engine wear. New gasolines were developed in concert with engine manufacturers trying to get the lead out but maintain the lifespan of engines.

- Fuel economy. Expensive gasoline led to minimizing transportation costs so gasoline changed and the engine manufacturers worked together collaboratively to change fuel mileage.

- Low temperature emissions at startup, and high temperature emissions (vapors). Some states capture vapours at the pump. These were huge investments across every pump handle.

- LUST and MUST - Leaking Underground Storage Tanks and Managing Underground Storage Tanks.

- Eliminating small refineries from operation as they are not efficient enough to provide low cost gasoline/diesel and can be a site of environmental risk.

- Eliminating small gasoline stations to remove the environmental risk. Each new site requires a much higher capital spend.

- Oilsands have dropped their emissions by 35% already. It's never enough. Two new technologies along with many more being considered will continue to improve the emissions. Beating companies with oilsands facilities into foreclosure might not be the best tact, and perhaps it would be wise to help partner on the road to lowering emissions in these long life assets. Cheering on the successes of lowering emissions would be a welcome goal. Somehow when Apple made much smaller improvements with computers, it was world-awakening.

- Flaring is being reduced significantly, and has been dropping for years. There is no appreciation for the gains already made.

- Carbon Capture and Storage will be extremely expensive. It has been going on for years, but the volume of capture is increasing dramatically and will need funding.

Drilling and Completions

- What about the drilling process? The price of oil has been dropping since 2008. Many oil service companies were wiped out. They ordered new equipment, but were not able to service the debt. They laid off staff, retired experienced people, and hunkered down for one of the longest drops in oil prices on record. In the face of environmental hatred towards the industry, new employees do not want to apply. I sent my nephew a job opportunity in the oilpatch as a recent business grad, and he couldn't be bothered to apply as the industry is in decline. The industry is out of favor with our youth, due to the social stigma. Is that a win for consumers or a problem? We have few new entries into the industry for drilling expensive new wells.

- Drilling has changed from vertical wells to horizontal wells. This requires new drilling rigs and more technical specialists on drilling the well, and the safety standards have improved immensely. All this adds complexity, and the days of moving a drilling rig around quickly from hole to hole is difficult.

- Drilling is one part of the new well process, but well completions are another whole deal. With horizontal wells, the cost of each well has gone up, the payback is quick, but not easy, and the decline rates of production are extremely fast. Figuring out the shelf life of compressor stations and production facilities is very important. But we lost the technical expertise building these gathering facilities in the slowdown.

- You can't send a fracking crew out without massive training, as the working pressures are enormous. We have no one trained because the low prices caused them all to lose their jobs. This is not the bunny rabbit reproduction model for rolling out new staff. It is time-consuming and expensive, with significant turnover in employees due to the remote work, the unsheltered work in the cold weather and the heat, as well as the competition hiring good people away after they get up to speed.

- Connecting these new production facilities requires small pipeline permits to connect to new or existing compressor stations nearby. These compressor stations clean up the oil to get it in a gathering system, where it goes down main pipelines to refineries.

Permitting

- In the old days you applied for a vertical well, and just needed the oil to be directly below. Now, with the advent of horizontal drilling, you may have multiple landowners including the government, First Nations, individuals, corporations that all own something along the way. Each one of those have to agree to the terms and the governments have tried to slow drilling. The 9000 un-drilled permits may have a host of logistical and permitting problems to be dealt with before they can proceed. They also need to connect the well to other infrastructure via pipelines and route the natural gas that comes up with the oil to processing facilities as well. This all takes time. The federal governments in the USA and Canada are insistent on downsizing the oilpatch because demonizing the industry is popular with their electorate. So slowing permits for onshore or offshore drilling is one way to control that.

- In the old days, permitting a well went through a series of filing steps in the office and after the approvals, the permit was granted. Now the geologist, geophysicist, drilling engineer, completions engineer, safety manager, land person, environmental specialist, First Nations communications, finance and senior management all need to have this one particular drilling area as their highest priority to garner the capital and attention to get it through to a successful permit application. This takes a lot longer than it used to. Usually many permits are needed from each area before you get "the permit".

- No one wants drilling or fracking in their back yard. NIMBY (not in my back yard). No one wants pipelines in their backyard. No one wants the oil industry in their backyard. Oil fields off the coast of California, Seattle and the west coast of Canada have been undeveloped due to the environmental pushback as energy costs soar. The new projects for the east coast are getting similar resistance.

Safety, Training, Environment

- Remember the Red Adair days of putting out wildfires on oilwells? Safety and training is a massive cost before a well can be drilled.

- New safety systems, deep training, and environmental cleanliness have all added to well costs and rightly so. Conversely, shutting in non-performing wells is expensive to clean up and return the site to a safe non-oil condition. All of these costs are now part of the modelling and they are significant hurdles to new development.

- The protection of the environment is one of the largest costs to the oil business and that is an important way of doing business to the employees inside the company as well. It has recently ramped up to include Carbon capture as just one of many things.

- Obviously I could spend days writing this area of the article. I won't bother as people who don't want oil and gas to succeed will always hope for failure or closure.

Summary

Why did I pen this article out in an article that Gas Prices Have Topped This Week? Because the lack of crude oil in the world is a big reason for rising prices over the last two years. Not two-weeks, but two years. The real problem is the always present protest community continues to successfully suppress the industry, especially in Canada and USA. In my opinion, it is going to be a long time before oil prices and gasoline prices normalize.

The focus on the oil and gas industry is immense. Low cost energy wasn't a benefit to the masses, and the supply of oil was a problem socially. Now the high prices of energy aren't a benefit to the masses, and the supply of oil is a problem.

This won't be solved by grandstanding. Only 25 million barrels /day of the 100 million barrels per day are used for transportation. We'll still need 75 million barrels a day for all the other things we make like clothing, containers and more. This is climbing every year.

Conclusion

I don't expect the volume of crude to increase even if Russia is allowed back on the world economic platform, until we deal with the reality of allowing new supply to come on stream since the downfall of oil and gas in 2020. It is interesting to hear that people are happy to pay a little more to take down Russia's aggression. However, they don't feel the same about paying more to reduce the carbon footprint of oil usage. When governments do tax the carbon, they don't return the money to the oilpatch for carbon capture or mitigation. Somehow it ends up wasted in general revenues, not protecting the environment. This is especially clear in Canada with rising carbon taxes each year.

Until then, I remain in the camp we are going to see higher prices as crude availability wanes. I think substantially higher prices are on the way until we come to grips with the reality of having oil companies as a helpful partner in our lives. Is that a stretch or what? That probably suggests how high prices can go.

The most successful countries in the world have had access to affordable energy for long periods of time. If oil prices don't drop, it will slow our economies, as it has for the last 100 years. We are going to need to model that into our future and continue to work towards that success. By iteratively getting better at lessening the damage to the environment each year, perhaps the citizens of the world can be seen supporting the improvements being made and allow the products to flow that we enjoy every day, including plastics, clothing, and mobility. Of the oil being produced, it would be good to focus on buying from areas with environmental legislation, a track record of continuous improvement and a stable government that supports development.

I am not sure you can get all three in one place, which outlines the difficulty of creating supply in the oil business.

Good trading,

Greg Schnell, CMT, MFTA

Senior Technical Analyst, StockCharts.com

Author, Stock Charts For Dummies

Want to stay on top of the market's latest intermarket signals?

– Follow @SchnellInvestor on Twitter

– Connect with Greg on LinkedIn

– Subscribe to The Canadian Technician

– Email at info@gregschnell.com