“The market will pull back about 5% before continuing higher.”

“The market will pull back about 5% before continuing higher.”

“Banks always do well with a steeper yield curve.”

“If the market moves higher, then gold will definitely pull back.”

“I’m sure we’ll see a correction in the next two weeks.”

When I was in college, one of my least favorite courses was Chemistry 202. This was second-year chemistry, which involved an extensive lab period. Mine was Tuesday and Thursday evenings from 6:30-9:30pm (only a college student would schedule something that insane).

I was not a good chemistry student. Don’t get me wrong, I could learn material very well and I could memorize formulas just fine. But chemistry started being more about being precise with lab equipment, which was certainly not my strong point.

Once, I stored my chemicals the wrong way, causing them to mix together and eat through the bottom of my drawer into the one below. Another time, I created something that started frothing over the counter and wouldn’t stop until the professor came over to resolve the issue. Both true stories.

But the most challenging day for me had to do with zinc iodide.

You see, one of our experiments was to follow a complex series of tests to identify which compound we had in our secret beaker. I ran out of time that class, so, at every subsequent class for two months I would have to finish the current experiment early so I could go back and keep trying to figure out what was in my secret beaker. After many failed attempts, missteps and wrong answers, I finally went up front and sheepishly said, “Zinc iodide?”

The lab assistant was so excited for me she actually hugged me. No kidding.

My point of this story is that, in this chemistry experiment, there was one right answer. There was a process to follow and there was only one accurate conclusion. My secret compound was not “maybe” zinc iodide, or “likely to be” zinc iodide, it was absolutely and undeniably zinc iodide.

Professor Andrew Lo often speaks of the “physics envy” of finance, where we want there to be these immutable laws that govern how stock prices fluctuate. Anyone who has spent five minutes trading knows that that's just not the case. As investors, we never deal with absolutes. We deal with probabilities.

If you’re looking for a technical indicator that will always give correct signals, you’ll be chasing a mirage. It doesn’t exist. What technical analysis does tell you is the probabilistic outcome based on historical trends and analysis. Over time, I’ve found it to be an additive to the investment process.

So, back to the quotes at the beginning of the article. What’s wrong with all of these statements?

They imply a certainty, a precision, an infallibility to the analytical process that just isn’t reality. They suggest that as an analyst, I know what will happen. That’s just not true - not for anyone. The best I can do is tell you what I think will most likely happen based on the evidence I’m reviewing.

So why do we make statements like these in the first place? Because we want to believe that the answer can be known. We want to believe that it’s possible to be right all the time. Even when the evidence tells us it’s impossible, we still want to believe it.

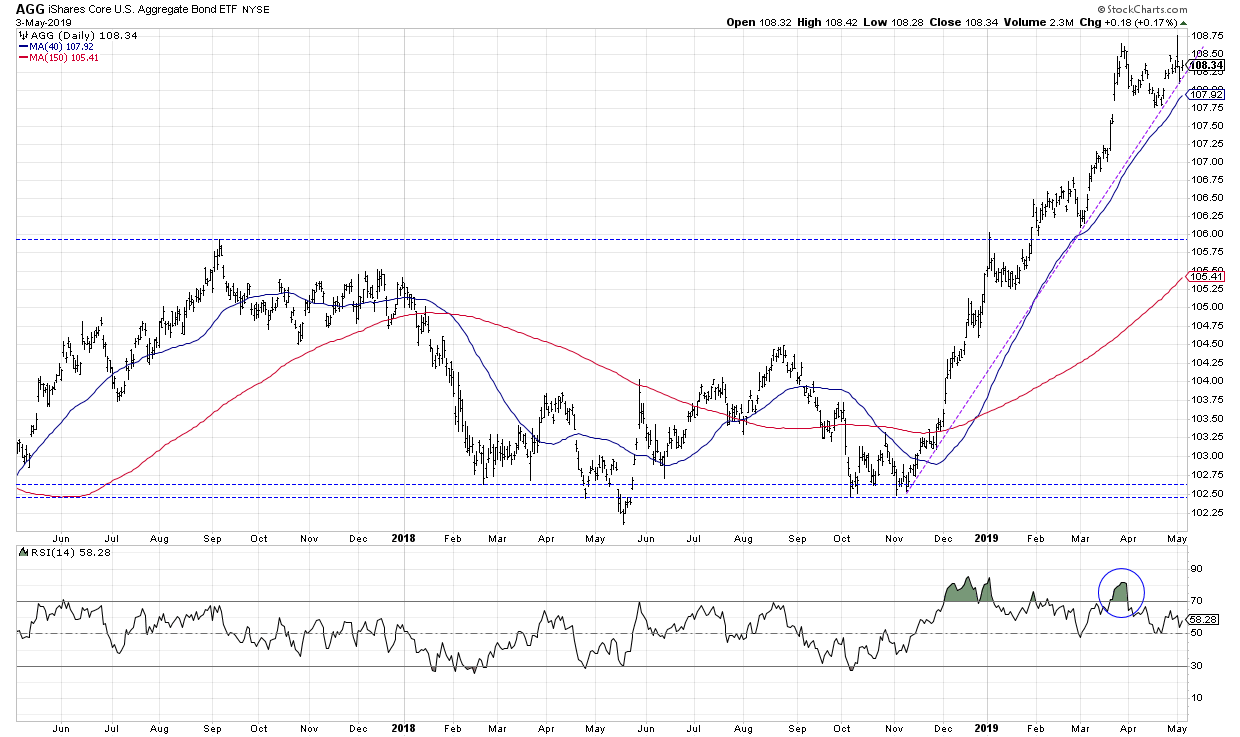

The fixed-income markets provide a perfect illustration of this phenomenon.

When ETFs like AGG became extremely overbought in late March, I developed the following thesis: bond prices will likely pull back from the overbought condition, but, due to the extreme overbought levels, I would expect one more push higher before price moves meaningfully lower.

That last point is based on the long-term transition from a falling rate environment (1980-2012) to a low rate environment (2012-2018) to a higher rate environment (2019-????).

I use phrases like “likely” instead of “definitely” and “I would expect” instead of “I know” to acknowledge the fact that I don’t know. No one does. What I do know is that charts provide the best opportunity to gauge where trends will likely evolve based on history, psychology and sentiment.

So if you catch yourself using words like "always" and "never" when describing an investment thesis, remember to think of technical signals in terms of the probability of the subsequent market movement, not the certainty of it.

RR#6,

Dave

David Keller, CMT

President, Sierra Alpha Research LLC

Disclaimer: This blog is for educational purposes only and should not be construed as financial advice. The ideas and strategies should never be used without first assessing your own personal and financial situation or without consulting a financial professional.

The author does not have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author and do not in any way represent the views or opinions of any other person or entity.