Market Recap for Monday, April 18, 2016

All nine sectors rallied on Monday to support the Dow Jones' breakout above the psychological 18000 barrier. Energy (XLE) and consumer discretionary (XLY) led the broad-based rally with gains of 1.65% and .94%, respectively. Healthcare (XLV) tacked on a .93% gain. A current chart of the XLE is provided in the Sector/Industry Watch section below. Among consumer discretionary areas, automobiles were particularly strong, rising 1.80% and breaking out of a bullish wedge. Check it out:

The blue line marks the start of a short-term uptrend and the timing is interesting as the DJUSAU tends to perform exceptionally well during the month of April. Check out the Historical Tendencies section below for more details.

The blue line marks the start of a short-term uptrend and the timing is interesting as the DJUSAU tends to perform exceptionally well during the month of April. Check out the Historical Tendencies section below for more details.

On a relative basis, industrials (XLI) lagged badly, rising just .09%. Airlines ($DJUSAR) and railroads ($DJUSRR) were the primary culprits as both finished the session in negative territory. Surprisingly, however, truckers ($DJUSTK) led the XLI with a gain of 1.05% nearly breaking out above 560 in the process. The divergence there is quite weak, though, so even a breakout will need to be viewed with caution.

Pre-Market Action

Light guidance seemed to be the issue with IBM after it reported its latest quarterly results after the bell on Monday. Subscriber growth was the issue with Netflix (NFLX). Both companies beat top and bottom line Wall Street estimates, but are under pressure this morning with losses of 4% and 9%, respectively. Still, rising crude oil prices ($WTIC) have traders on a high note once again this morning as U.S. futures have shaken off the disappointing headline earnings from last night and push higher.

U.S. equities also appear to be shaking off weaker than expected housing data as both housing starts and building permits came in much weaker than expected.

Asian markets were strong overnight with the Nikkei's 3.7% gain completely reversing its big losses the previous session. In Europe, the German DAX is making a very notable breakout well above the 10000 level this morning. The S&P 500 tends to track German shares closely so this morning's 2.2% gain should not be ignored.

Current Outlook

The Dow Jones closed above 18000 yesterday for the first time since July 20th. Volume on the breakout, however, was light and the Dow is currently printing a negative divergence on its 10 minute, 60 minute and daily charts. So it's difficult to fully embrace this rally. But maintaining a bearish stance hasn't exactly been working out either. Still, signs of slowing momentum is always a concern. Yesterday, I provided a daily chart showing the MACD rolling over on the Dow Jones. Check out the 60 minute chart, which also shows momentum in the very near-term to be weak as well:

Note the 20 hour EMA held as support on the most recent selling episode. I'm not expecting that on the next bout of selling. Instead, the rising 50 hour SMA is now at price support. Look for the Dow Jones to weaken enough to test both of these levels - at a minimum.

Note the 20 hour EMA held as support on the most recent selling episode. I'm not expecting that on the next bout of selling. Instead, the rising 50 hour SMA is now at price support. Look for the Dow Jones to weaken enough to test both of these levels - at a minimum.

Sector/Industry Watch

Energy (XLE) again bounced strongly off its 20 day EMA despite crude oil prices ($WTIC) moving lower over the weekend. The XLE remains the best performing sector in 2016. Like many areas of the U.S. stock market, a negative divergence on the XLE daily chart is issuing a short-term warning sign, but volume has been solid, offsetting those momentum issues. Take a look:

There has been considerable price resistance in the 65 area so it would be best to see a breakout there before committing additional capital to the group, but I expect to see energy continue to lead the S&P 500 on a relative and absolute basis.

There has been considerable price resistance in the 65 area so it would be best to see a breakout there before committing additional capital to the group, but I expect to see energy continue to lead the S&P 500 on a relative and absolute basis.

Historical Tendencies

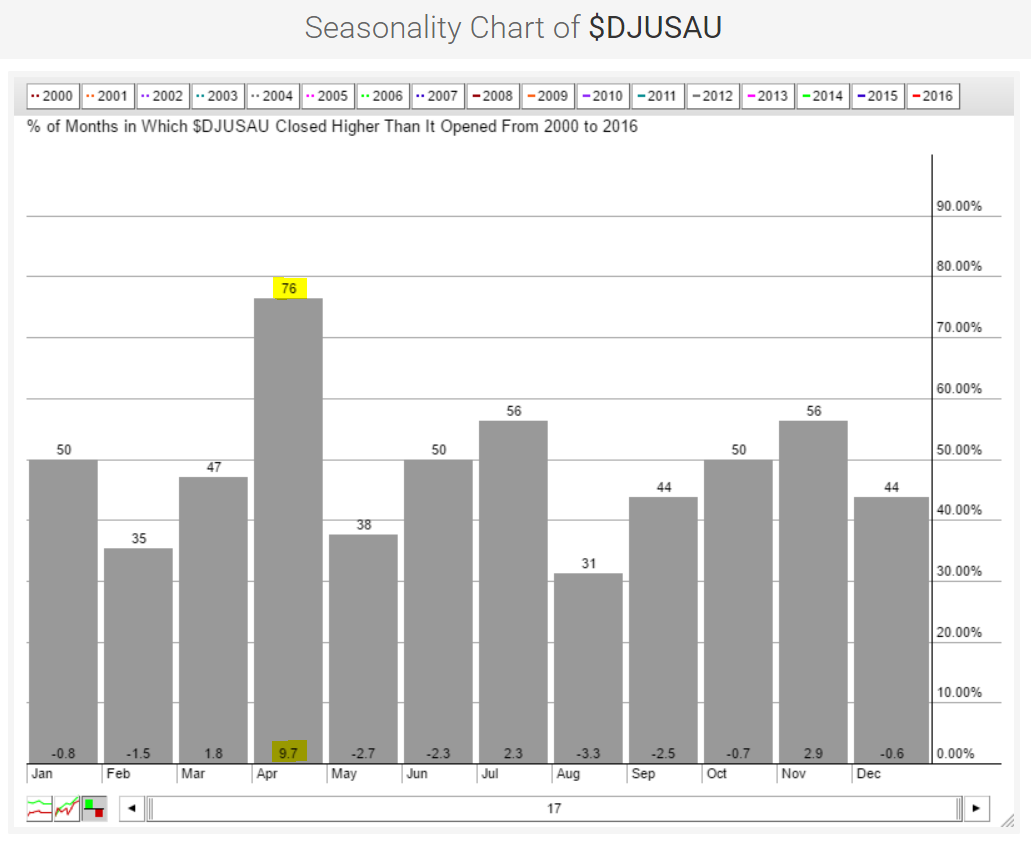

As mentioned above, automobiles ($DJUSAU) love the month of April. On the seasonality chart below, you can see that autos perform MUCH better in April than any other calendar month:

In terms of average monthly returns, April's 9.7% average return is more than triple its next best calendar month performance in November where average gains are just 2.9%.

In terms of average monthly returns, April's 9.7% average return is more than triple its next best calendar month performance in November where average gains are just 2.9%.

Key Earnings Reports

(actual vs. estimate):

AMTD: .38 vs .38

CMA: .34 vs .42

GS: 2.68 vs 2.57

HOG: 1.36 vs 1.28

JNJ: 1.68 vs 1.64

NTRS: 1.01 vs .95

PM: .98 vs 1.11

UNH: 1.81 vs 1.72

(reports after close, estimate provided):

DFS: 1.30

INTC: .49

ISRG: 3.46

VMW: .58

YHOO: (.02)

Key Economic Reports

March housing starts released at 8:30am EST: 1,089,000 (actual) vs. 1,167,000 (estimate)

March building permits released at 8:30am EST: 1,086,000 (actual) vs. 1,200,000 (estimate)

Happy trading!

Tom