Market Recap for Tuesday, January 31, 2017

It was a second day of rotation into defensive stocks as leadership came from healthcare (XLV, +1.60%), utilities (XLU, +1.55%) and consumer staples (XLP, +0.48%). Unfortunately, all of the aggressive sectors were lower and that kept a lid on overall price action. Our major indices finished in bifurcated fashion mostly because of a very strong last two hours yesterday afternoon on the NASDAQ and Russell 2000. The latter actually finished with solid 0.70% gain, while the large cap Dow Jones closed beneath 20000 for the second consecutive session after ending three straight days above that psychological level. A primary reason for the Dow Jones lagging was the horrible action in transportation stocks ($TRAN). Has the group completed a handle?

Typically, the handle doesn't drop below 50% of the cup itself, but the TRAN has seen a drop of slightly more than 50%. So if you're trading this as a cup with handle, you need to see a quick reversal followed by a breakout above 9500 on heavy volume.

Typically, the handle doesn't drop below 50% of the cup itself, but the TRAN has seen a drop of slightly more than 50%. So if you're trading this as a cup with handle, you need to see a quick reversal followed by a breakout above 9500 on heavy volume.

Pre-Market Action

The bulls are set up for a solid day so far in pre-market action. Global markets are mostly higher, especially in Germany where the German DAX ($DAX) is rebounding strongly after closing below its 20 day EMA on Tuesday - the first such occurrence since early December. The DAX is up 1.25% currently.

The ADP employment report came in much stronger than expected with 246,000 jobs vs. the estimate of just 168,000. That's sent the 10 year treasury yield ($TNX) up nearly 4 basis points to 2.49%.

Finally, Apple (AAPL) delivered the strong results that the technology bulls were hoping for as its EPS came in at 3.36, well above the 3.22 consensus estimate.

With 30 minutes left to the opening bell, Dow Jones futures are higher by 73 points with action on the NASDAQ much stronger thanks to AAPL.

Current Outlook

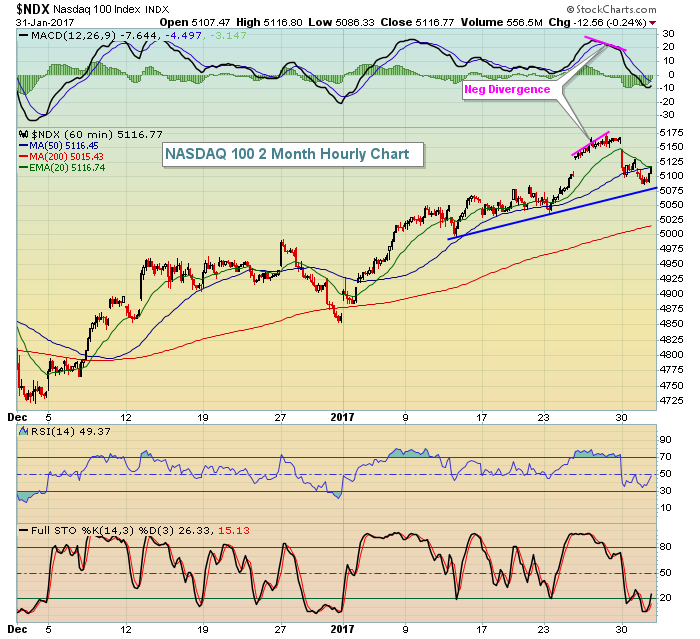

On the heels of a solid earnings report from Apple (AAPL) last night after the closing bell, the NASDAQ 100 appears ready for another advance to challenge its recent high:

This non-financial, heavily weighted technology index showed signs of slowing momentum in the form of a negative divergence last week. That was rectified by recent weakness, however, and given AAPL's bullish reaction to its earnings report last night, I'm looking for the strength in the NDX back near 5175. The beginning of calendar months tend to be very bullish and that simply adds another layer of short-term bullishness to the current outlook for U.S. equities.

This non-financial, heavily weighted technology index showed signs of slowing momentum in the form of a negative divergence last week. That was rectified by recent weakness, however, and given AAPL's bullish reaction to its earnings report last night, I'm looking for the strength in the NDX back near 5175. The beginning of calendar months tend to be very bullish and that simply adds another layer of short-term bullishness to the current outlook for U.S. equities.

Sector/Industry Watch

The market didn't exactly like the United Parcel Service (UPS) earnings report as the reaction on Tuesday was very poor. As a result of a 6.75% drop in UPS shares, the Dow Jones U.S. Delivery Services Index ($DJUSAF) lost short-term price support and appears to be heading for a lower support level. Check out the index:

The volume was very heavy on the short-term breakdown, but I'm expecting to see the group hold onto support near 920. The trading range for now is 920-960.

The volume was very heavy on the short-term breakdown, but I'm expecting to see the group hold onto support near 920. The trading range for now is 920-960.

Historical Tendencies

The first day of ALL calendar months tends to be the best day historically to be in the stock market on the long side. Money flows drive prices higher - not always as I'm talking tendencies here. Consider this: the S&P 500 has risen 53.3% of all trading days since 1950. But on the first calendar day of the month, this percentage rises to 61.22%. The annualized return on the first calendar day is +46.17%, by far the best of any calendar day.

Key Earnings Reports

(actual vs. estimate):

ADP: .87 vs .81

ANTM: 1.76 vs 1.59

BAX: .57 vs .52

CAJ: .26 vs .55

CE: 1.52 vs 1.51

D: .99 vs 1.00

IR: .84 vs .92

JCI: .53 vs .51

MO: .68 vs .67

MPC: .43 vs .25

PPL: .60 vs .52

(reports after close, estimate provided):

ALL: 1.61

AVB: 2.10

EW: .71

FB: 1.13

LNC: 1.71

MET: 1.34

NXPI: 1.41

SYMC: .21

TSCO: .92

UNM: .98

Key Economic Reports

January ADP employment report released at 8:15am EST: 246,000 (actual) vs. 168,000 (estimate)

January PMI manufacturing index to be released at 9:45am EST: 54.3 (estimate)

January ISM manufacturing index to be released at 10:00am EST: 55.0 (estimate)

December construction spending to be released at 10:00am EST: +0.2% (estimate)

Happy trading!

Tom