Market Recap for Wednesday, June 19, 2019

Yesterday was Fed day, or Fednesday as one MarketWatchers LIVE viewer said, and U.S. equities liked what the Fed had to say. What it had to say was essentially what most market pundits were expecting - that the word "patient" would be removed from the Fed's policy statement and that the likelihood of an upcoming rate cut would be apparent. After the meeting, fed funds futures implied that we will see a rate cut when the Fed meets again in July.

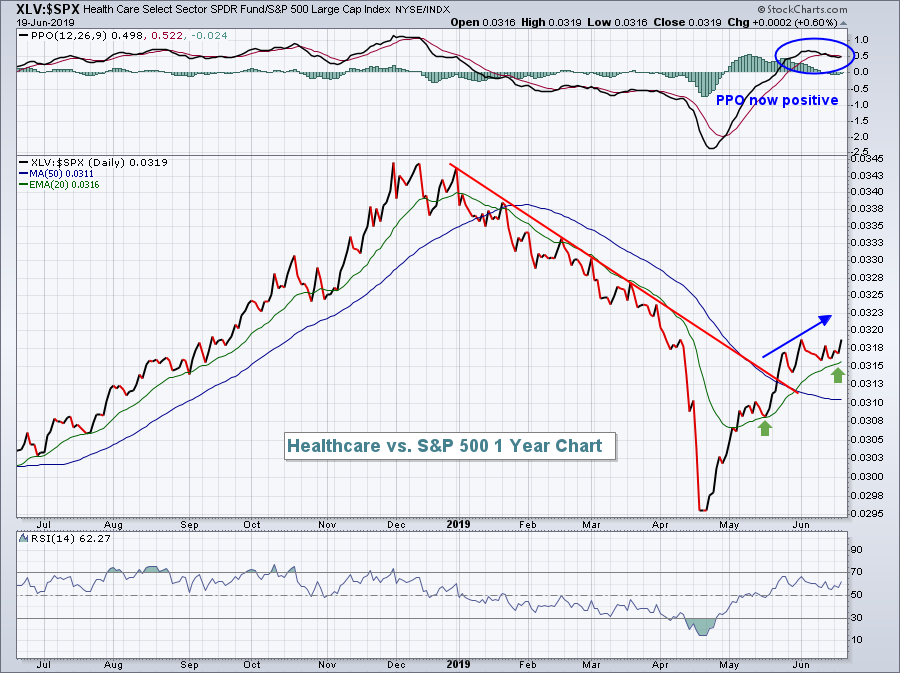

All of our major indices gained ground on Wednesday, albeit the gains were small. Leading the action was the NASDAQ, which jumped 0.42% and with a notable spike after the Fed's 2pm EST statement. The biggest negative to come out of yesterday's gains was the fact that defensive groups were in charge of the rally. Healthcare (XLV, +0.90%), utilities (XLU, +0.76%), real estate (XLRE, +0.66%), and consumer staples (XLP, +0.41%) were the leaders. If that combination were to continue driving the overall market higher, we'd need to grow more cautious.

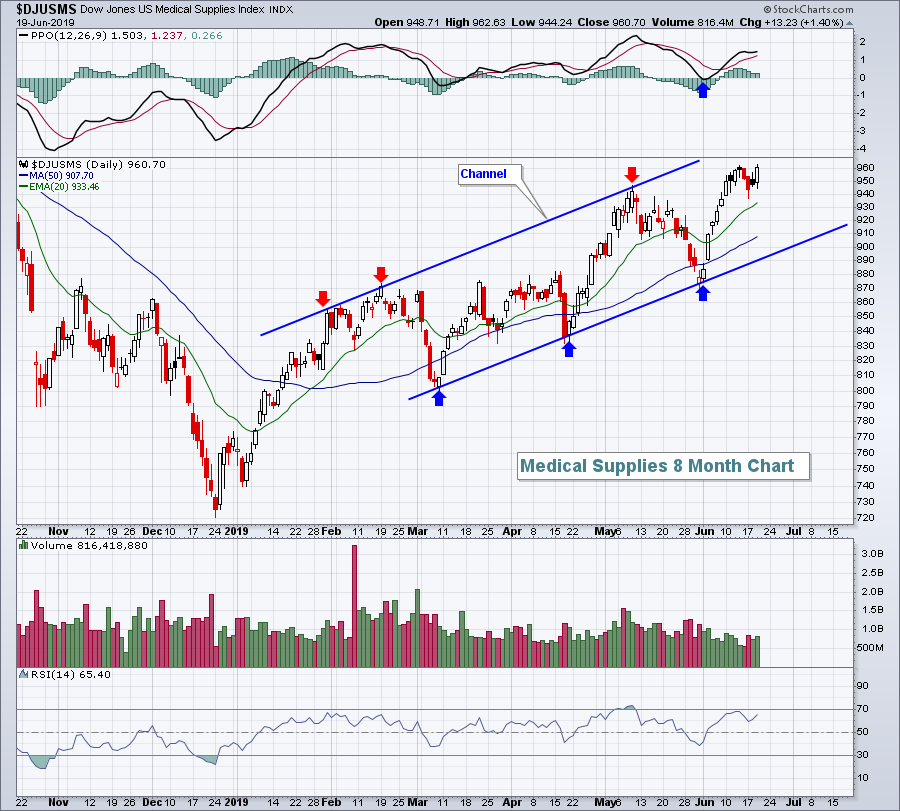

Medical supplies ($DJUSMS, +1.40%) was an outperformer yesterday and its technical improvement continues:

The channel is very well-defined with multiple tests of channel resistance (red arrows) and channel support (blue arrows). It was also bullish to see the PPO turn higher off centerline support. I expect to see further strength in medical supplies, especially since healthcare tends to perform very well during the summer months.

The channel is very well-defined with multiple tests of channel resistance (red arrows) and channel support (blue arrows). It was also bullish to see the PPO turn higher off centerline support. I expect to see further strength in medical supplies, especially since healthcare tends to perform very well during the summer months.

Special Note

Subscribing to my blog is completely FREE. If you enjoy my articles, simply scroll to the bottom of this article and type in your email address in the box provided. Click on the green subscribe button and VOILA! All of my articles will be sent to the email address you provide immediately upon publishing. Thanks so much for your support! :-)

Pre-Market Action

U.S. equities are showing further strength this morning with Dow Jones futures higher by 235 points 30 minutes before the opening bell. But nothing is hotter this morning than gold ($GOLD), which is soaring 2.7% to $1386 per ounce, its highest level in 5 years. The prospects of the Fed turning more dovish is a bearish signal for the U.S. Dollar ($USD). Should the USD weaken further, it'll provide tailwinds for GOLD. A breakout on GOLD above $1400 per ounce could prove extremely bullish. Keep one thing in mind, however. While GOLD is likely to move higher, we still want to review its relative strength vs. the S&P 500 as the SPX is moving higher as well. GOLD is very likely to move higher in my opinion, but can it outperform the S&P 500? That will be the question I want answered.

Global markets are rallying, as is crude oil ($WTIC), which is up above $55 per barrel this morning.

Current Outlook

Healthcare (XLV) has a tendency to outperform the S&P 500 during the weaker stock market months of May through August. The XLV's relative strength turned at the end of April, almost right on cue:

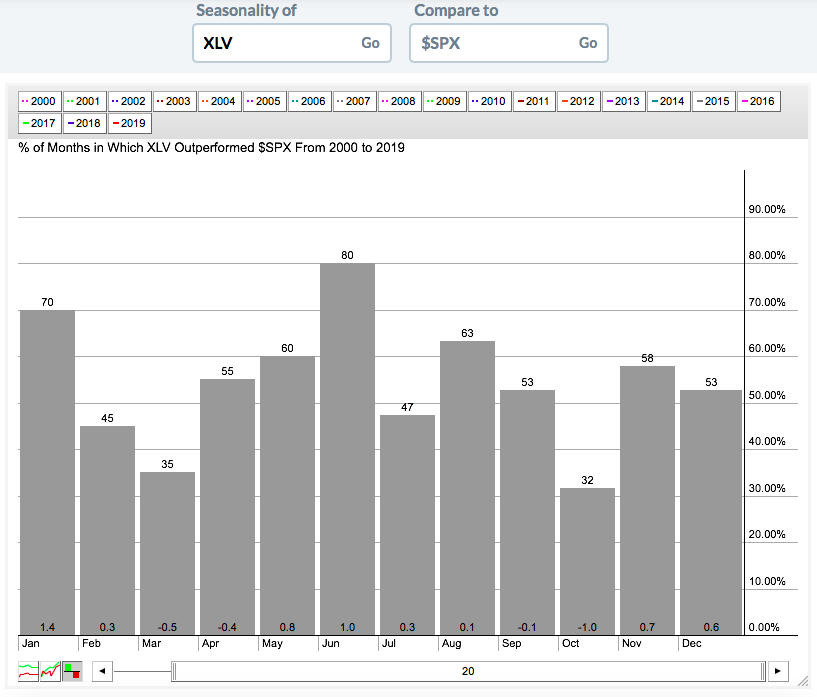

The XLV has a history of outperforming the S&P 500 over the past couple decades and that can be seen here in this seasonality chart:

The XLV has a history of outperforming the S&P 500 over the past couple decades and that can be seen here in this seasonality chart:

You can see that the XLV has outperformed the SPX in 80% of Junes this century. While its relative strength during the other summer months isn't quite as strong, the XLV does outperform in those months as well.

You can see that the XLV has outperformed the SPX in 80% of Junes this century. While its relative strength during the other summer months isn't quite as strong, the XLV does outperform in those months as well.

Sector/Industry Watch

The Dow Jones U.S. Travel & Tourism Index ($DJUSTT, +1.70%) had a very nice day on Wednesday, but in the words of The Carpenters, "We've Only Just Begun". There's work to do, but breakouts on both absolute and relative bases would be an excellent start. As mentioned in Historical Tendencies below, we're set to enter a historically bullish period in July, but I'd want to see technical improvement first:

The downtrend line in the top part of the chart has been tested on multiple occasions over the past year and failed every single time. Also, note that any short-term relative strength enjoyed by the DJUSTT has not lasted and has been followed by another major relative downtrend. The red arrows mark the key points along the absolute downtrend, while the black arrows mark the relative reaction highs when the group bounces. If the DJUSTT can clear the downtrend line and the recent relative reaction highs, we could see much more relative strength over the balance of the summer.

The downtrend line in the top part of the chart has been tested on multiple occasions over the past year and failed every single time. Also, note that any short-term relative strength enjoyed by the DJUSTT has not lasted and has been followed by another major relative downtrend. The red arrows mark the key points along the absolute downtrend, while the black arrows mark the relative reaction highs when the group bounces. If the DJUSTT can clear the downtrend line and the recent relative reaction highs, we could see much more relative strength over the balance of the summer.

As we can see from the chart, however, that's a very big "IF".

Historical Tendencies

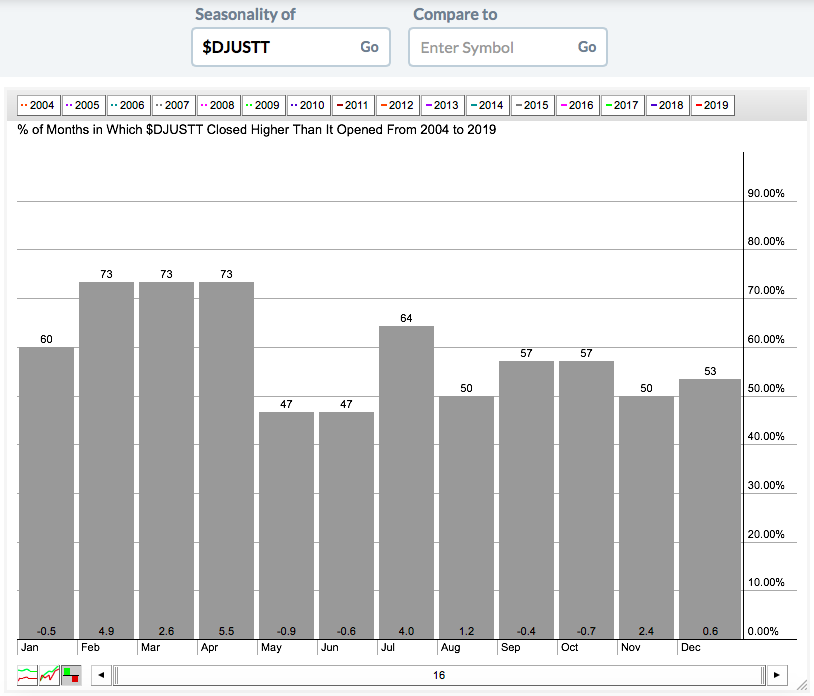

The July to September period has been challenging for U.S. equities historically, but there are a few bright spots. For instance, the Dow Jones U.S. Travel and Tourism Index ($DJUSTT) has risen in each of the last 7 years and sports a nice average return over the past 16 years:

That average July return of 4.0% trails only April (5.5%) and February (4.9%) as the group's best calendar month.

That average July return of 4.0% trails only April (5.5%) and February (4.9%) as the group's best calendar month.

Key Earnings Reports

(actual vs. estimate):

CMC: .67 vs .63

DRI: 1.76 vs 1.73

KR: .72 vs .71

(reports after close, estimate provided):

CGC: (.17)

KFY: .89

RHT: .85

Key Economic Reports

Initial jobless claims released at 8:30am EST: 216,000 (actual) vs. 220,000 (estimate)

June Philadelphia Fed survey released at 8:30am EST: 0.3 (actual) vs. 11.0 (estimate)

May leading indicators released to be released at 10:00am EST: +0.1% (estimate)

Happy trading!

Tom