Market Recap for Friday, June 14, 2019

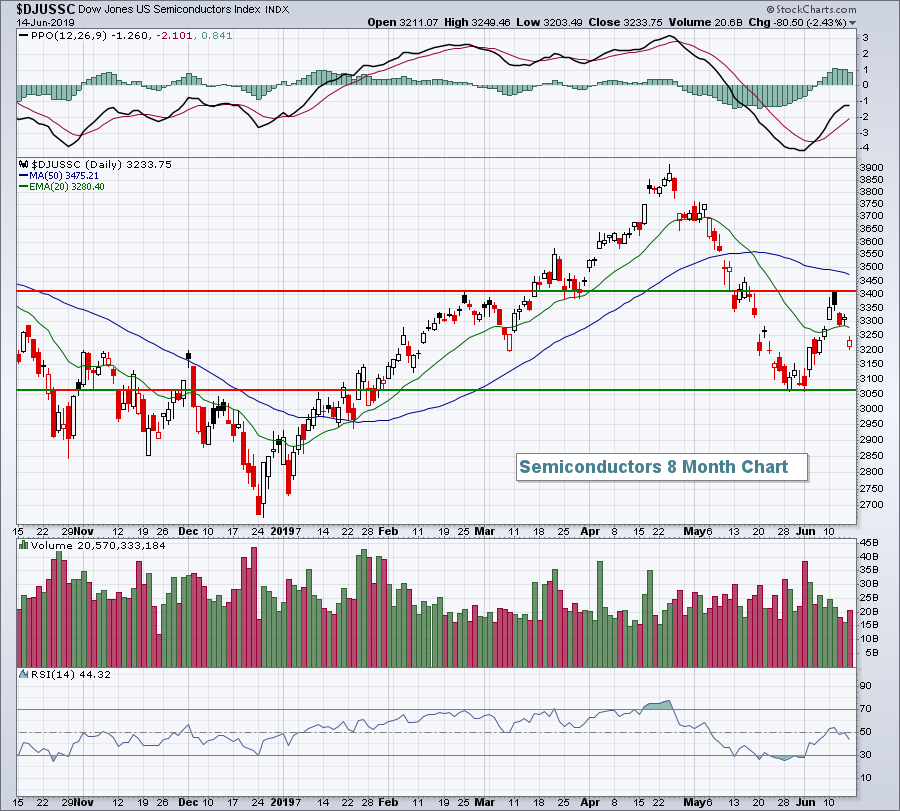

The big news on Friday was Broadcom's (AVGO, -5.57%) quarterly results and outlook, neither of which were particularly good. AVGO fell short of its revenue estimate and offered a very broad warning regarding upcoming revenues in the semiconductor industry ($DJUSSC, -2.43%). The DJUSSC lost its rising 20 day EMA, a bearish development, and now traders have their eyes set on the price support established by the late-May low:

The weakness in semiconductors weighed on technology (XLK, -0.87%) as that sector was the worst performing group. It also weighed on the NASDAQ, which lost 0.52%, more than the corresponding losses on the S&P 500 and Dow Jones, which totaled 0.16% and 0.07%, respectively. Still, the volume on the DJUSSC wasn't nearly as heavy as I would have expected and buyers seemed to emerge at the opening bell to support the group on Friday. The worst may have been built into semiconductor stocks, however, as that May low is holding - at least for now. If the U.S. stock market is to move higher from here, it would seem reasonable to expect that the semiconductors will need to continue to hold onto support from May.

The weakness in semiconductors weighed on technology (XLK, -0.87%) as that sector was the worst performing group. It also weighed on the NASDAQ, which lost 0.52%, more than the corresponding losses on the S&P 500 and Dow Jones, which totaled 0.16% and 0.07%, respectively. Still, the volume on the DJUSSC wasn't nearly as heavy as I would have expected and buyers seemed to emerge at the opening bell to support the group on Friday. The worst may have been built into semiconductor stocks, however, as that May low is holding - at least for now. If the U.S. stock market is to move higher from here, it would seem reasonable to expect that the semiconductors will need to continue to hold onto support from May.

Utilities (XLU, +1.05%) and real estate (XLRE, +0.43%) - two defensive sectors - led Friday's action.

Pre-Market Action

The 10 year treasury yield ($TNX) is flat this morning, despite a weaker-than-expected empire state manufacturing survey report. Gold ($GOLD) is also flat, while crude oil ($WTIC) is lower by 0.42% to $52.29 per barrel.

Asian markets were fractionally higher, while European markets are mixed this morning.

Dow Jones futures are up by 22 points as we get set to kick off another trading week.

Current Outlook

After failing to make its attempted breakout last Tuesday, the S&P 500 has simply traded sideways and consolidated. I see a short-term trading range from gap support at 2873 to the weekly high in the 2900-2910 range:

Let's see which level gives way first.

Let's see which level gives way first.

Sector/Industry Watch

Home construction ($DJUSHB, +1.25%) broke out again on Friday amidst the falling interest rate environment. The 10 year treasury yield ($TNX) reeling to 2.09% and near a multi-year low is beneficial to the group and it has shown:

The green arrow highlights the PPO bounce off centerline support, which supports the bullish uptrend. If there's one negative, it's the lack of volume on Friday to confirm that breakout. Failure to hold the breakout would likely lead to a 20 day EMA test.

The green arrow highlights the PPO bounce off centerline support, which supports the bullish uptrend. If there's one negative, it's the lack of volume on Friday to confirm that breakout. Failure to hold the breakout would likely lead to a 20 day EMA test.

Monday Setups

Great Lakes Dredge & Dock Corp. (GLDD) printed a shooting star candle a little over a week ago, highlighting the importance of exiting a short-term trade when this occurs with a false breakout:

The heavy volume throughout the recent advance is encouraging and likely represents accumulation. While there's still possible downside to the 9.75-10.00 range, the recent selling is setting up a very solid short-term reward to risk trade, especially if we see a further decline. I like a price target of 11.25-11.40 with entry at 10.20 and 9.75. A closing stop beneath 9.65 could be considered.

The heavy volume throughout the recent advance is encouraging and likely represents accumulation. While there's still possible downside to the 9.75-10.00 range, the recent selling is setting up a very solid short-term reward to risk trade, especially if we see a further decline. I like a price target of 11.25-11.40 with entry at 10.20 and 9.75. A closing stop beneath 9.65 could be considered.

Historical Tendencies

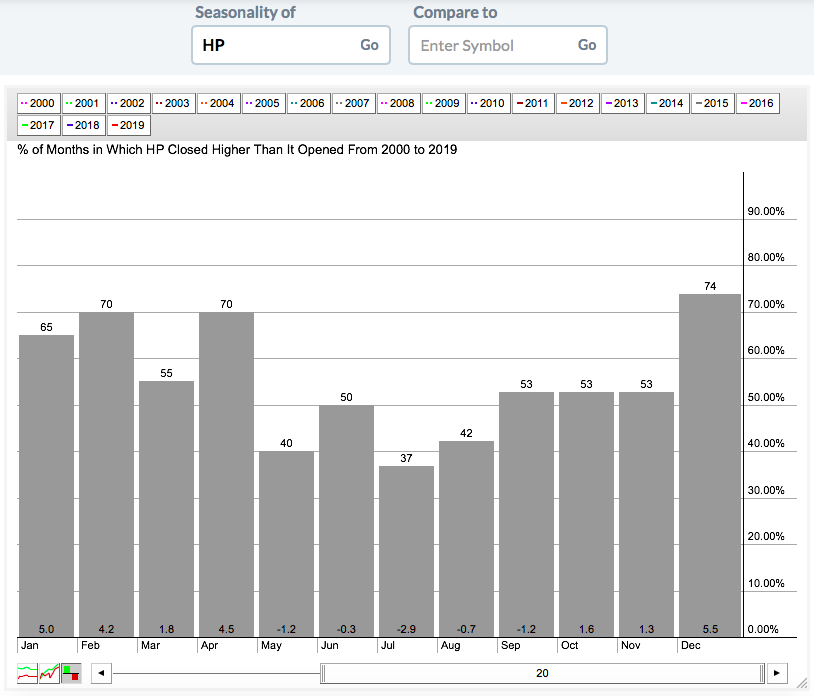

Helmerich & Payne (HP) is battling against two big foes. First, its peer group has been very weak as the Dow Jones U.S. Oil Equipment & Services Index ($DJUSOI) has dropped nearly 48% over the past year. Second, the summer season has been brutal for this stock over the past two decades:

HP has averaged gaining 23.9% from October through April during the past two decades. Unfortunately, we're not in that time period right now. Instead, we're in the midst of the May through September period when HP has averaged falling 6.3% over those same 20 years. Its worst month - July - has yet to come. Check out the last 6 years:

HP has averaged gaining 23.9% from October through April during the past two decades. Unfortunately, we're not in that time period right now. Instead, we're in the midst of the May through September period when HP has averaged falling 6.3% over those same 20 years. Its worst month - July - has yet to come. Check out the last 6 years:

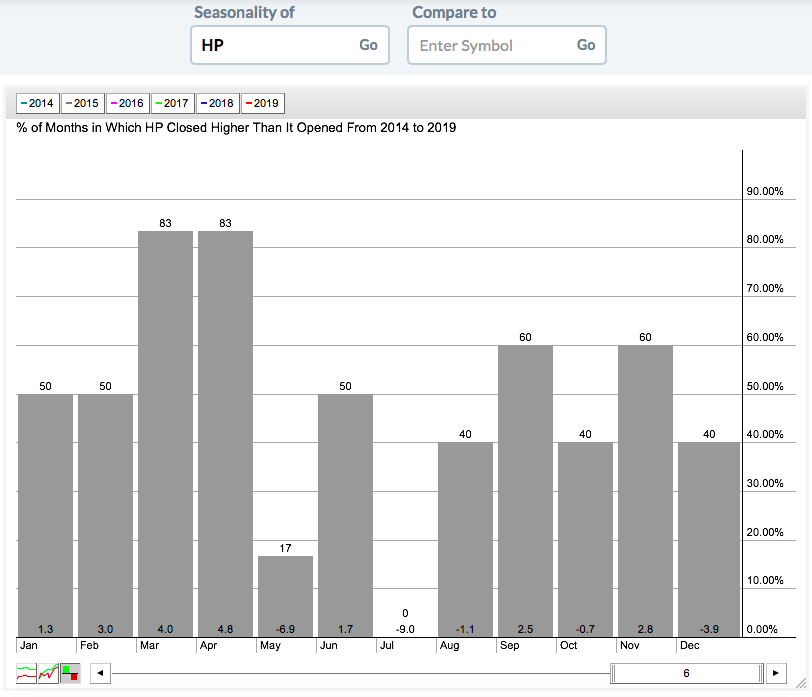

July hasn't seen a winning month in the past six. And it's averaged losing 9% per July.

July hasn't seen a winning month in the past six. And it's averaged losing 9% per July.

Key Earnings Reports

None

Key Economic Reports

June empire state manufacturing survey released at 8:30am EST: -8.6 (actual) vs. +10.0 (estimate)

June housing market index to be released at 10:00am EST: 67 (estimate)

Happy trading!

Tom